The rise in interest on student loans

Rise in interest on student loans

In October of this year, the announcement was made that the interest rate on Dutch student loans will rise to 2.56 percent per January 1, 2024. Given the current rate of 0.46 percent, the interest percentage will increase fivefold. The increase has evoked a wide outcry amongst students, especially amongst students of the so-called ‘bad luck generation’. This generation is the category of students that studied between 2015 and 2022 and that fell subject to the abolishment of the basic grant system while also being confronted with an increase in interest rates. As of 2023, the basic grant system was reintroduced. According to the Central Statistical Office (CBS), more than 1.6 million people had a student loan debt by the beginning of 2023. At this moment, the average student debt in The Netherlands is around €17,100.00.1

In general, most students feel like there are two major problems with the increase. The first and most obvious one is that the increase will imply a substantial additional amount of interest that has to be paid back. Secondly, some students note that they feel insufficiently informed by the Dutch government about the terms and conditions of this loan. According to them, the loan has been portrayed as an interest-free loan, mostly because the interest rate has been at 0 percent for multiple years. Students took on a loan under the impression that it will stay this way, and this turned out not to be true. The goal of this article is to explain the background of the increase and to give you insight into what else could have been done.

The Dutch government has linked the interest of student loans to five-year Dutch government bonds. Governments can choose how to determine the interest rate on study loans. There are a few factors that determine a government's choice. One important consideration is that the interest on loans must be based on something that is stable and does not usually fluctuate too often. Generally, bonds would fit this criterion as they experience little volatility. Another consideration is that of the government budget. To finance the demand for study loans, governments can sometimes issue bonds. Linking the interest on study loans to these bonds could therefore be a logical choice.

Across the world, governments handle the student loan systems differently. In the USA, student loans are linked to federal debt obligations, more specifically Treasury bills, and the interest rate on those loans is determined by the ten-year Treasury note auction plus a fixed increase with a cap. The current interest rate on federal undergraduate student loans is 5.50 percent.2 In the UK, the interest rate is based on the Retail Prices Index (RPI) and has been capped since September 2023 due to high inflation.3

How has interest on Dutch government bonds developed?

To track the evolution of interest rates on Dutch government bonds, we should examine the inflation and interest rates set by the European Central Bank (ECB). The primary objective of the ECB is to uphold price stability, accomplished by targeting an inflation rate of approximately 2%. This goal can be decomposed in two different subgoals, which are both essential to a well-functioning economy and monetary system. First, expectations and trust influence how well a monetary system operates. By keeping prices relatively predictable, both consumers and corporations have reasonable expectations about their future purchasing power and their decision to save and invest money. Secondly, by keeping the inflation rate around 2% specifically, the ECB also aims to protect the Eurozone economies from deflation. Deflation is undesirable in an economy as it will procrastinate spending. Since consumer spending is a major driver of economic growth, deferred spending will have major negative consequences and can create a downward spiral. A rate of 2% on average also allows countries within the Eurozone to naturally fluctuate around this rate, without relying on countries to experience deflation.4

To achieve the monetary policy goal of price stability, any central bank can influence inflation in different ways. The most conventional approach (therefore called conventional monetary policy) is to influence the interest rates, which essentially determine the “price of money” and therefore inflation. The ECB has three key interest rates which are part of monetary policy.5 The first key interest rate is the main refinancing rate: the rate at which commercial banks can borrow money from the central bank on the intermediate term (from 2 weeks to 3 months). The rate at which commercial banks can borrow money also determines the rates at which commercial banks can lend money. This is important as this is one of the main ways this rate trickles down to the customers of the bank, which make up the real economy. The second key interest rate is the marginal lending rate; the rate at which commercial banks can borrow money in the short term. The third and last key interest rate is the deposit interest rate. This is the rate that commercial banks earn when they store reserves at the central bank. If this rate is higher, it is more attractive for commercial banks to hold onto excess reserves, i.e. any reserves above the minimum required reserves, than to lend out money to their customers. This effect is similar to the effect of the main refinancing rate.

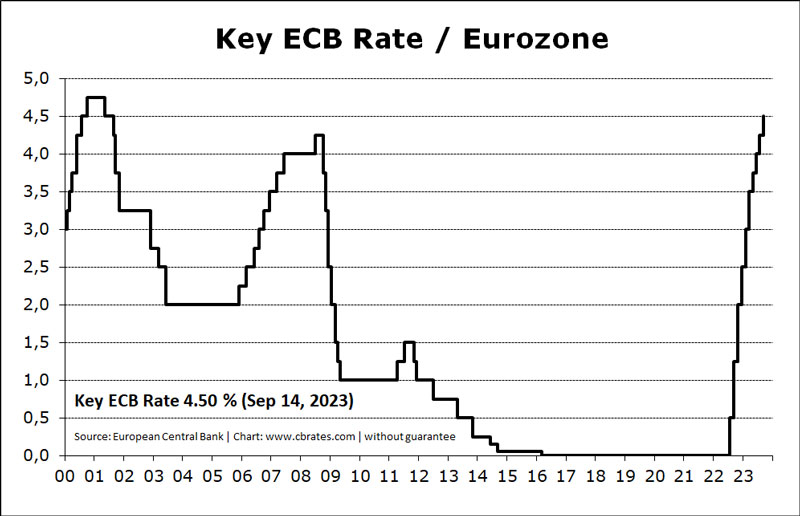

Now that we understand the mechanisms of monetary policy, we can revert back to the key discussion of why interest rates on study loans have increased so much in the last year. As mentioned earlier, this rate is linked to the interest rates on Dutch government bonds. To give context to this development of interest rates, we will look at the table below.6

Figure 1: Key ECB Rate per year in the Eurozone

The student loan system was introduced in 2015. Around these years, the interest rates were at an ultra-low point or at zero. During this period, there was a large amount of savings in the economy due to the aging of the population.7 Additionally, there was less demand for loans from the economy. On top of that, inflation was low so the central banks had no incentive to increase interest rates to counteract inflation. In 2022, the Eurozone experienced periods of ultra-high inflation, reaching a level of almost 10%. The inflation experienced in the Eurozone was most likely due to forces outside monetary policy: the covid-period led to major supply chain and workforce disruptions, and energy prices rose significantly in this period. Although these could be considered as unexpected and external forces, it is in the ECBs interest to try to counteract inflation by monetary policy; i.e. raising the interest rates. This is exactly what happened in the last year: for the first time in 11 years, the ECB raised the interest rates. It can likely be stated that these disruptions and their consequential monetary policy could never be expected in earlier years when the student loan system was introduced.

What are the alternatives to government bonds? What are the plans of political parties to change this?

Even with an understanding of why interest rates have changed, not everybody agrees that these higher interest rates should also be translated down to student loans. When the news was announced, many Dutch students went to protest and it has been of great debate in the country. Earlier last year, an interest increase has been announced from 0% to 0.46%.8 Now with an increase to 2.56%, many students are worried. Not only does it simply amount to larger installment payments, students feel that it is unfair that they enter into a loan agreement without knowing the interest payment beforehand. The interest has to be paid retroactively on the amount that was borrowed before, but at the time of borrowing that money, the interest payment was unknown. Some students also claim that the interest increase poses a threat to the accessibility of higher education.

Now with a governmental election coming up, many political parties have taken a stance on the issue. Some parties, including BIJ1, Partij voor de Dieren and DENK have pleaded for an interest rate that stays at 0%. BBB pleads for zero interest on existing student debt. Many other parties, like VVD, Groenlinks - PvdA, Nieuw Sociaal Contract and Volt have not taken the stance of a rate of 0%, but do mutually agree on an interest rate that is capped or at least very low. Some parties are less focussed on the interest rate directly, but want to encourage ex-students to amortize quicker via a discount. People that are able to amortize on their loan quicker, will eventually pay less interest in that way. CDA and ChristenUnie are in favor of this idea.

Conclusion

In conclusion, the announcement of rising interest rates has caused discussion throughout society. However, the higher interest rate to a certain extent does not come out of the blue. At the time the student loan system was introduced, the worldwide economy was in a different stage with an exceptionally low-interest rate of (nearly) zero. In recent years, the ECB has increased the interest rate due to high inflation and their monetary policy goal of price stability. Because of their link to government bonds, student loans experience the consequences of these developments. The interest rate on student loans is a big topic for students and therefore relevant with regards to the Dutch government elections this month. Several political parties have already declared that they want to prevent students from paying the 2.56% interest. The last word on student debt interest rates may not yet have been spoken, and we will follow the developments with great interest.

Sources

1. Centraal Bureau voor de Statistiek. (2023, October 10). Studieschuld opgelopen tot 28 miljard. Retrieved from CBS

2. J. Smith. (2023, September 21). Student loan interest rates. Investopedia. Retrieved from Investopia

3. Student Loans Company. (2023, August 2023). Student Loans Interest Rates and Repayment Threshold Announcement. Gov.UK. Retrieved from gov.uk

4. European Central Bank. (2021, November 18). Waarom zijn stabiele prijzen belangrijk? Retrieved from ECB

5. N. (2023, September 15). The ECB’s key interest rate: what it is and how it affects you. N26.

6. Central Bank Rates | Worldwide Interest Rates | European Central Bank (ECB). (n.d.) CBR

7. Rente. (n.d.). DNB

8. NOS. (2023, October 9). Rente op studieschuld vanaf volgend jaar meer dan vijf keer zo hoog. NOS.